|

Dr. P.V. Viswanath |

| Courses/ FIN 649 | ||

Exams |

||||||||||||||||||||

|

|

||||||||||||||||||||

| Midterm Exam Notes:

1. (25 points) Please define any five of the following terms:

2. (30 points) Please answer any three of the following questions:

3. Mexicana de Cobre had been borrowing from the Mexican government at a high rate. In order to avoid these high borrowing rates, it arranged to borrow $251 million from a consortium of 10 banks at a fixed rate of 11.48%. Here is how the deal was arranged (this case is described in more detail in Managing Financial Risk: A Guide to Derivative Products, Financial Engineering, and Value Maximization by C.W. Smithson, C.W. Smith, Jr., and D.S. Wilford (Chicago: Irwin Professional Publishing); note that the details there differ in some details from the details given here). The picture below was taken from the web at http://www.trinity.edu/rjensen/caseans/133sp.htm#Sogem :

A Belgian company, Sogem, agreed to purchase 3700 tons of copper per month (presumably for the duration of the loan) at the prevailing spot price for copper. However, the payments from Sogem went not to Mexicana de Cobre, but rather to an escrow account in New York. Funds in the escrow account were then used to service the debt, and any residual was returned to Mexicana de Cobre.

4. a. (10 points) The Oz Forex Foreign Exchange site provided the following quotes (https://www.ofx.com/en-au/exchange-rates/) around 12:30 on Monday, November 1, 2004.

The AUD/USD quote is a direct quote from the American point of view, while the USD/CAD quote is an indirect quote from the American point of view. Compute the cross-rate between the Australian dollar and the Canadian dollar. b. (10 points) The Oz Forex Foreign Exchange site provided the following foreign exchange quotes (https://www.ofx.com/en-au/exchange-rates/) around 12:30 on Monday, November 1, 2004.

Discover arbitrage opportunities, if any, if the EUR/JPY quote were 135.65/135.8. c. (10 points) According to http://quotes.tradingcharts.com/futures/quotes/ED.html, the current (around 1 p.m., Nov. 1, 2004) 3-month Eurodollar futures price for the March 2005 contract is 97.765. Suppose you go long a contract at this price. Suppose further that the closing/settlement price tomorrow is 97.90. How much money would you have to pay/ would you receive, given that the contract has a principal value of $1m. (Source: http://www.cme.com/trading/prd/overview_ED3087.html) 5. (15 points) The Economist of Oct. 28, 2004 in its article, "The wolf at the door: A further steep decline in the dollar seems inevitable," says the following: MOST economists, and this newspaper, have been fretting about America's huge current-account deficit and predicting the dollar's sharp decline for years. The trouble with crying wolf too often is that people stop believing you. After slipping 14% in broad trade-weighted terms since 2002, the dollar had stabilised this year, even as the current-account deficit continued to grow. This has encouraged some economists to offer theories explaining why America's current-account deficit does not matter and why the dollar need not fall further. But the dollar has now started to slide again: this week it hit $1.28 against the euro, within a whisker of its all-time low of $1.29. Trust us, the wolf is real. The dollar's latest slide seems to have been triggered by uncertainty about the presidential election and a flurry of comments from Fed officials. Robert McTeer, the president of the Dallas Federal Reserve, mused (only “theoretically” of course) that when capital inflows into America dry up, “there will be a crisis that will result in rapidly rising interest rates and a rapidly depreciating dollar that will be very disruptive”. Explain why the uncertainty about the presidential election and the "flurry of comments" should have caused the dollar to drop. 1.

2. a. A forward forward is an agreement to transact at a future date at a fixed pre-determined price. With a forward forward, when the contract matures, the parties consummate the agreed-upon transaction. In a forward rate agreement, the transaction is not consummated at the maturity date; rather, there is an exchange of money to compensate the parties. If necessary, any spot transaction is done separately. b. The advantage of a currency board is that monetary policy is not within the control of the central bank. As a result, investors do not have to worry about the government running deficits and monetizing them, or otherwise cheapening the currency by increasing the money suppply. c. It could borrow in euros and then take a long position in euros in the futures/options markets to benefit from the expected appreciation of the euro (assuming that this appreciation has not already been incorporated into exchange rates). Alternatively, it could borrow in dollars and speculate on the dollar depreciating. d. If the Chinese yuan appreciates against the dollar, the competitive position of US exports to China would improve. Hence the position of the traded goods sector in the US would improve. e. Governments might intervene in the foreign exchange markets for various reasons: one, they might desire an overvalued domestic currency, so as to have lower import prices and potentially lower prices for imported consumer goods; two, they might desire an undervalued currency, so as to improve employment in the traded goods sector; three, they might believe that the currency is mispriced and desire to correct it, so as to provide correct signals to firms making investment decisions. 3. a. By having the deal go through the escrow account in New York, the banks would have a lien on the money, as soon as it reached the escrow account. And since Mexicana de Cobre is in the copper producing business, there is little chance that it would not have copper to deliver on the Sogem deal. The political risk of the Mexican government intervening and stopping payments on the debt would be reduced. b. The banks could eliminate the risk of the copper price dropping by doing selling copper short in the futures market. If the price of copper rose, the banks would lose money on the futures contract but would be assured of a sufficiently large sum of money from the SOGEM purchase. If the price of copper dropped, there may not be enough money in the escrow account, but there would be a profit in the futures market. Alternatively, the banks could buy a put option in the copper market. Finally, they could enter into a swap, where they would pay the floating price based on the spot copper market, and receive a fixed price from the counterparty. 4. a. A$1 can purchase US$0.7459, which can be converted into C$(0.7459)(1.2224) or C$0.9118. C$1 can purchase US$(1/1.2229), which can buy A$(1/1.2229)(1/0.7464) or A$1.0956. Hence to get A$1, you need to give up CA(1/1.0956) or C$0.9128. Hence the bid price for the A$ in Canada is C$0.9118, while the ask price is C$0.9128. b. 1 euro can buy US$1.2738, which can buy (1.2738)(106.36) or 135.48 yen, which, in turn can be converted into 135.48/135.9 euros, which is less than 1 euro. However, 100 yen can buy US$(100/106.41), which can buy (100/106.41)/1.2743 euros, i.e. 0.73747 euros. These can be sold for (0.73747)(135.65) or 100.038 yen, which is a profit of .038 yen per 100 yen. Hence, there is an arbitrage opportunity, and it can be availed of by using yen to buy dollars, using the dollars to buy euros and then using the euros to buy yen again. c. The futures price of 97.765 implies a contract value of $1m/(1+(100-97.765)/400) or $994,443.36. A futures price of 97.90 can be computed in the same way to be worth $994,777.40. Hence, an investor who is long the Eurodollar futures contract will get $334.12 5. The uncertainty about the presidential election means that there is

uncertainty about future economic policies, which means that there is

uncertainty about the future value of owning a dollar. The comments, of

course, suggest and could trigger a rapid depreciation of the dollar,

in case it starts to slide. In other words, this increases the volatility

of the dollar, which again reduces the desirability of being exposed to

the dollar. This would cause the dollar to drop, right now. Notes:

1. (18 points) Please define any six of the following terms:

2. (30 points) Please answer the questions below based on the following excerpt from The Wall Street Journal of Nov. 9, 2004:

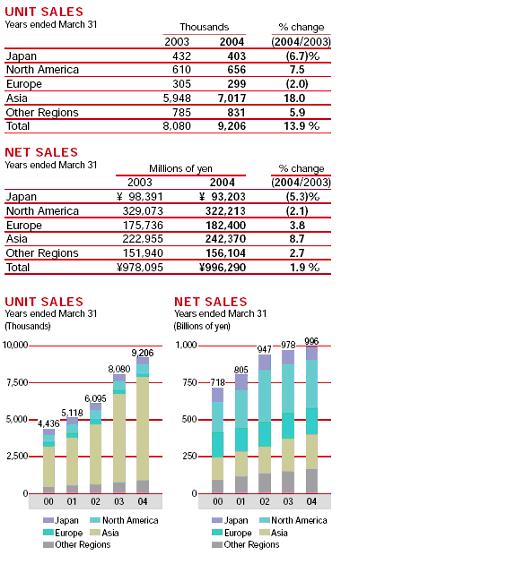

You also have available to you, Honda's corporate profile and some information on Honda's worldwide sales CORPORATE PROFILE WSJ, Nov. 9, 2004: TOKYO (Nikkei)--Honda Motor Co. (7267.TO) will spend about Y30 billion to build a new factory in Georgia that will begin producing automatic transmission systems as early as 2006, the Nihon Keizai Shimbun reported Tuesday. The construction plan comes as the company is expanding output of automobiles,

such as its Pilot sport utility vehicle and Odyssey minivan, in the neighboring

state of Alabama. Honda's annual vehicle production capacity has reached 1.4 million units in North America. Although the company locally procures almost all of the engines needed to assemble these automobiles, local production of automated transmissions - a key component of vehicles that requires a huge investment in production due to their complicated structure - did not start until 1996. The company currently produces 1 million transmissions annually at its Ohio factory in the U.S. Midwest - in which its major automobile plants are concentrated - and imports the remainder from Japan. Q. 3. (12 points) Answer any one of the following questions, a. or b.:

Q. 5. (30 points) Answer any three of the following questions:

Q. 6. Read the following article from the Dow Jones Newswires on Nov. 15, 2004 and answer the following questions:

BUENOS AIRES (Standard & Poor's) Nov. 15, 2004--Standard & Poor's Ratings Services today assigned its 'B' local and foreign currency corporate credit rating to the 1,000-MW, hydroelectric generator Chivor S.A. E.S.P. in Colombia. The outlook is positive. At the same time, Standard & Poor's assigned its 'B' rating to the company's upcoming US$150 million 10-year 144A senior secured notes to be issued in November 2004. The ratings reflect Chivor's weak expected debt service coverage for 2005 and 2006 within a context of volatile cash generation that mirrors the largely hydro-based Colombian electricity system. The ratings also incorporate a limited degree of financial flexibility after the company restructured its debt in August 2002. These weaknesses are partly offset by the company's portfolio of power sales contracts mainly with local electric distribution companies at a fixed price in Colombian pesos and indexed by local inflation. In addition, Chivor is a low cost generator in Colombia's electric system and benefits from a relatively large dam and a favorable hydrology within its region, although it faces significant competition from other large hydro generators. Chivor's 1,000-MW plant is projected to generate an average of about 4,000 gigawatt-hours (GWh) per year, from which about 2,500 GWh are expected to be sold through short-and medium-term sales contracts (of up to three years) and the remaining 1,500 GWh marketed in the volatile spot market. Chivor's main revenue and cash flow sources are power sales under contracts, spot market sales, capacity revenues, and, to a lesser extent, revenues from ancillary services such as frequency control. Chivor's current indebtedness is composed of a US$260 million outstanding bank loan that matures in 2006. The upcoming US$150 million, 10-year secured fixed rate bond and a Colombian peso 260 billion (about US$100 million), seven-year amortizing syndicated bank loan will be used to refinance the outstanding loan, significantly extending Chivor's debt maturity schedule and lowering the company's exposure to foreign exchange risk. 1.

2. (Note that the chart/table provided in the exam actually refers, not

to automobiles, but motorcycles; this was an inadvertent mistake. I will

evaluate your questions based, obviously, on the information given to

you -- even if it might be factually incorrect.) Given that Madison is short drachma and there is a positive correlation between the lira and the drachma, Madison should create a long position in lira; that is, Madison should buy lira forward. According to the regression, a 1¢ change in the value of the lira leads to a 1.6¢ change in the value of the drachma. To cross-hedge the forthcoming payment of Dr, Lit 1.6 must be bought forward for every unit of Dr owed. With a drachma exposure of Dr 250 million, the exporter must buy forward Lit in the amount of Lit 400 million (1.6 x 250,000,000).

|