Industry Analysis and Top-down investing

The Business Cycle and Investing

Top-down investing involves looking at trends in the general

economy and then selecting companies likely to benefit from those trends.

Implementation:

Look at the case of the countries in the Asian debt crisis (see M. Freddie

Reiss, "Asian Markets" in Dominic DiNapoli, ed. (1999) "Workouts

and Turnarounds II," 279ff.). Look at the

case of Enron, or at the case of other companies that have

"inexplicably" crumbled. In many of these cases, it is clear

that the fundamentals were not reflected in the prices. This suggests that

if one had looked at the fundamentals, one could have sold out in

time. Of course, this represents a certain sort of market

inefficiency. But this is a market inefficiency that favors fundamental

analysis. If we can assume that the same applies for the upside as well

(that is, by looking at fundamentals, we can find stocks/sectors that are

under-priced), we should look at the fundamentals.

In order to reduce the order of difficulty of our problem, let us divide our

approach into two parts -- one, finding a sector/industry that is under-priced,

and then select stocks within those "under-priced" sectors that are

underpriced relative to the sector and relative to other stocks, as a whole.

Sector Selection:

How can we select sectors? In principle, there is no reason why our

approach to sector selection should be different from our principle to stock

selection. Although we are yet to discuss stock valuation and stock

selection, there are some basic principles that apply in both stock selection,

as well as sector selection. We could use those same principles to select

sectors. However, the difficulty with this approach -- one, we would need

to get a lot of information on cashflows, since the basic stock valuation

approach that we will use is cashflow based; and we will need a lot of

detail. Hence I will suggest an alternative approach.

We know that the economy is down quite a bit -- most of the statistics are

pretty bad. If we can agree that the economy is not likely to keep going

down in the medium term (in the short term, maybe), then, even if we do not know

when the upturn will occur, the sectors that will do well, when the upturn does

occur will be sectors that have the flexibility to capitalize on the new

opportunities. (And, actually, many of the measures of flexibility that we

will look at, will not hurt firms even if the economy continues going down.)

What aspects characterize a flexible firm? I can think of two -- one, a

low debt-equity ratio; and two, lots of free cashflow that are available to make

NPV>0 investments.

Cash flows:

Let's look at cash flows; let's see if there are industries that have a

high level of free cash flow. Whereas when the economy is flush, an excess

of free cash flow might lead firms to make bad investments, at times like these,

an availability of free cash flow is advantageous -- the firm/industry will have

cash when good investments become available. (Read article

on dividends from the Economist.).

In fact, we might refine this approach further. Perhaps there are

industries that already have investment opportunities -- admittedly, there are

not going to be many of these, but we can look! If such industries exist,

then their capital expenditures may very well be rising. Of course, if

these industries are already investing in profitable opportunities, why would

the market not reflect that in their prices already? After all, even if we

are positing a certain level of market inefficiency, let's not assume gross

inefficiency! On the other hand, it would not hurt to use this factor as a

secondary selection criterion. If we have sectors that are making

investments, this suggests that their free cashflow is probably not

increasing. In fact, if free cashflow is increasing, that might very well

indicate that the sector is experiencing accelerating problems.

So let's look at industries where capital expenditures are increasing and/or

high as well as industries where free cash flow is high and decreasing

(indicating, usage).

Leverage:

Firms with high leverage have to worry about paying off their debt or at

least servicing it. This does not give them much flexibility to capture

investment opportunities. Furthermore, debt, in general, and in these

times, in particular, is probably laden with restrictions and covenants.

Hence, if we want flexible sectors, we want sectors with relatively low leverage

ratios; industries with low debt/equity ratios

(relatively) or industries where debt-equity ratios have not increased relative

to their historic averages, or at least where they have not trended up.

Of course, we would need to look at debt levels/leverage relative to other

industries. Of course, since it's not possible to simply compare leverage

across industries -- the fundamentals are different, we need to do a

cross-sectional regression of leverage ratios. Perhaps use Damodaran's

cross-sectional regression model -- let's see if, perhaps there are

industries that tend to have below average leverage. Again, low relative

leverage suggests the ability to survive, as well as to the flexibility to raise

funds if necessary.

Implications of Market Efficiency for Capital Budgeting

Market Efficiency is usually assumed only for capital markets, because there

is relatively free flow of information. However, this is not assumed in

the market for real assets/projects. In other words, we assume that firms

can pick NPV>0 projects, even though, in general, we do not make that

assumption for (active) portfolio managers. However, this does not mean

that all projects will be NPV>0. Alan Shapiro has the following

insights (in an HBS article)

A project can be reliably identified as being positive NPV only if we can

also identify the sources of that positive NPV. In general, the sources of such

value enhancement represent some deviation from perfect competition in the

product market, such as the existence of barriers to entry in the firm's

industry, due to:

- the availability of economies of scale in production

Lesson: Investments that are structured to exploit economies of scale are

more likely to be successful than those that are not.

- the possibility of product differentiation

Lesson: Investments designed to create a position at the high end of

anything, including the high end of the low end, differentiated by a quality

or service edge, will generally be profitable.

- cost advantages

Lesson: Investments aimed at achieving the lowest delivered cost position

in the industry, coupled with a pricing policy to expand market share, are

likely to succeed, especially if the cost reductions are proprietary.

- monopolistic access to distribution channels

Lesson: Investments devoted to gaining better product distribution often

lead to higher profitability.

- protective government regulation

Lesson: Investments in project protected from competition by government

regulation can lead to extraordinary profitability. However, what the

government gives, the government can take away!

________________________

The Business Cycle and Stock Selection (From Robert Arnott (Chap. 9) in Investment Management by Bernstein

and Damodaran)

Leading Indicators also provide an interesting gauge. If leading

indicators have risen in the past year, typical of a recovery from a recession,

we find that heavily leveraged companies and labor-intensive companies are

likely to do well. Typically, during the recession that precedes an upturn

in leading indicators, most labor-intensive companies have already cut costs;

they enter the new economic cycle lean and well-positioned for the ensuing

economic recovery. Also when leading indicators have risen in the past

year, growth stocks have likely already made their move; accordingly, the value

stocks (high earnings-to-price stocks) would tend to do particularly well.

In each of these cases, we are not looking at coincident relationships, but

predictive relationships. One might surmise that the market would already

have incorporated this information into stock prices, but that seems not to be

the case.

________________________

Sectors and the Business Cycle

http://www.fidelity.com.hk/sector/funds/guide/economic.pdf

Why a sector emphasis?

http://www.fidelity.com.hk/sector/funds/guide/benefits.pdf

Practical Matters:

How do we define sectors? We can do it in several ways -- one we use

the S&P definition of sectors; two, we use the StockVal

definition.

S&P Sector Dynamics, Oct. 2001 from Fidelity

sector.pdf

Sector and Style Investing

http://www.investors-routemap.co.uk/Guidebook_sector_rotation.htm

________________________

Information in Different Textbooks:

Chapter 13 of Jones:

A detailed listing of business cycle contraction and expansion dates can be

found at http://www.nber.org. Go to http://www.smartmoney.com/economywatch/

to find a set of nine important economic indicators, including data on sales,

earnings, exports, prices, and jobs. Monthly statistics on the leading

indicators as well as other indicators can be found at http://www.yardeni.com.

The Federal Reserve Banks have numerous details on various aspects of economic

activity and all of them can be accessed through any of the regional banks, such

as http://www.frb.clev.org. A daily

commentary on economic activity can be found in the "Research,"

"Economics," part of Lehman's website at http://www.lehman.com.

Chapter 17 from Bodie, Kane and Marcus

Key Variables describing the macroeconomy:

- Gross Domestic Product (GDP)

- Unemployment Rate

- Inflation Rate

- Interest Rates

- Budget Deficit

- Sentiment

Classify shocks as demand shocks versus supply shocks. Demand shocks

are events that affect the demand for goods and services in the economy.

Positive demand shock examples are

- reductions in tax rates,

- increases in the money supply,

- increases in government spending

- increases in foreign export demand.

Supply shocks are events that influence production capacity and costs.

Examples are:

- changes in the price of imported oil

- freezes, floods or droughts

- changes in the educational level of an economy's work force

- changes in the wage rates at which the labor force is willing to work.

Demand shocks are characterized by aggregate output moving in the same

direction as interest rates and inflation, while supply shocks have the opposite

effect.

Consider a given scenario and identify which industries/firms would be

benefited by that scenario.

Section 17.5 on the Business Cycle.

Cyclical Industries have above-average sensitivity to the state of the

economy; they would outperform the market when the economy is improving.

Examples are producers are producers of durable goods, such as automobiles or

washing machines; other cyclical industries are producers of capital goods.

Defensive industries include food producers and processors, pharmaceutical

firms and public utilities. These industries will outperform others when

the economy enters a recession.

Leading indicators from the Conference Board are:

- Average weekly hours of production workers (manufacturing)

- Initial claims for unemployment insurance

- Manufacturer's' new orders (consumer goods and materials industries)

- Vendor performance -- slower deliveries diffusion index.

- Contracts and orders for plant and equipment

- New private housing units authorized by local building permits

- Interest rate spread, 10 year Treasury minus federal funds rate

- Stock prices, 500 common stocks.

- Money supply

- Index of consumer expectations.

Look at http://www.conference-board.org/economics/index.cfm

for information from the Chief Economist, The Conference Board.

Also, look at Aaron Gottesman's notes (c:\class\smip\macroeconomy_ag.ppt)

How to analyze companies and industries: Sites and Sources

Data on the service-sector is provided by (ISM) Institute for

Supply Management's manufacturing report

Because sector funds have a narrow focus, the sector fund investor should be

familiar with the factors that may affect the industry in question. Based on a

comprehensive analysis of the relevant facts, the investor must arrive at a

judgment as to what the industry's performance will be like going forward. One

technique commonly used by sector fund investors is to monitor the business

cycle for clues as to what may be happening in the market.

Business cycle basics

In its most classic form, the business cycle involves a recession giving way

to modest growth, then stronger growth. Eventually, growth reaches a peak, and

a slowdown begins, leading to recession and a completion of the cycle.

By examining empirical evidence, the investor can attempt to create a

framework for viewing present and future events as they unfold. There are two

key questions the investor may want to ask about historical empirical

evidence. First, will the historic pattern hold, or will it be altered? To

answer that, the investor needs to ascertain whether the factors driving

today's market are fundamentally unchanged, or whether the situation has

evolved incrementally or even been radically changed.

The second question is whether the market has already taken the anticipated

future events into account. If the factors driving the industry are the

traditional cyclical ones, the market usually will have taken them into

account, because they are expected. If the factors represent a new element in

the equation, then the market may not be expecting them and may not have

adjusted accordingly.

Business cycle and relative stock performance

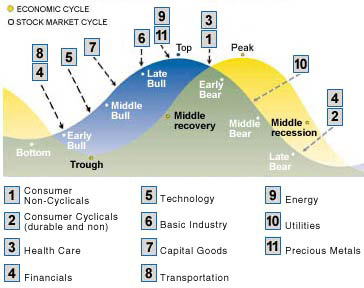

The following chart shows a typical business cycle and the points at which

various economic sectors tend to outperform the broader market. Click on any

number in the chart to learn about the cyclical characteristics of a

particular industry. Please note that the chart should be used for

illustrative purposes only. The chart is a historical representation of stock

performance movements relative to the business cycle and is not intended to

convey any current or future economic outlook.

Past performance is no guarantee of future results.

The chart above shows a typical business cycle and the points at which

various economic sectors tend to outperform the broader market. Please note

that the chart should be used for illustrative purposes only. The chart is a

historical representation of stock performance movements relative to the

business cycle and is not intended to convey any current or future economic

outlook. Choose a Sector for a detail description of its role in the business

cycle.

Consumer

Non-Cyclicals

Consumer

Non-Cyclicals

Stocks in consumer non-cyclicals (food) and consumer growth industries

(cosmetics, tobacco, beverages) tend to experience fairly steady demand and

are less sensitive to changes in the business cycle. These stocks typically

attract investors when the economic cycle or bull market has matured, or is in

the early stages of contraction.

Consumer

Cyclicals (durable & non)

Consumer

Cyclicals (durable & non)

Stocks in this category include durables and non-durables that are sensitive

to interest rates as well as the business cycle. Investors typically seek them

out when the economy is in the late stages of contraction.

Healthcare

Healthcare

In general, stocks in this sector move similarly to consumer non-cyclicals.

This sector is considered defensive, meaning companies in this sector are

generally unaffected by economic fluctuations. The Healthcare industry

consists of pharmaceutical firms, HMOs, biotechnology firms and medical

equipment suppliers. Pharmaceutical companies are affected by competitive

market shares, the pace of FDA approvals, patent lives, and the strength of

the R&D pipelines. Many biotechnology firms are still in the development

stage with their fortunes largely determined by investor perceptions of the

relative merits of their R&D pipelines. With future new financing likely

to be more difficult to obtain than in the past, strategic alliances between

major drug companies and biotech firms are expected to increase.

Financials

Financials

Stocks in housing-related industries tend to respond well to falling interest

rates and are often targeted by investors in the mid to late stages of an

economic contraction. Non-mortgage-dependent banks are generally driven by

commercial and consumer loan growth, and tend to be favored by investors

during the middle of the cycle.

Technology

Technology

Technology stocks can be cyclical to the degree that they depend on capital

spending and business or consumer demand. However, they may also have

long-term growth potential as technological products find broader applications

and as new technologies are developed. Technology stocks are usually popular

during early to mid stages of an economic expansion.

Basic

Industry

Basic

Industry

Profits of basic industries are driven by high utilization of capacity and

strong market demand for products. Therefore, their stocks tend to be popular

with investors late in an economic expansion. For basic material companies,

the global economic picture and supply/demand equation also affect stock price

movements.

Capital

Goods

Capital

Goods

Capital spending tends to increase midway through the business cycle, as the

economy is heating up and higher demand for products leads companies to expand

their production capacity. Demand in global export markets is key for

agricultural equipment, industrial machinery, and machine tools.

Transportation

Transportation

Railroads and other surface carriers tend to react early to a pickup in the

economy. Airlines are subject to cyclical fuel costs, usage versus capacity,

and competitive pressures on airfares.

Energy

Energy

This category includes large integrated international companies, domestic

exploration companies, and energy services companies. Each industry has its

own dynamics, but ultimately all are driven by the supply and demand picture

for energy worldwide. Political events have historically had a major impact on

these industries. Stocks tend to be popular with investors late in the

business cycle.

Utilities

Utilities

Electric companies have historically been very sensitive to interest rates

because of the large debt financing costs they must incur in order to build

their infrastructures. These stocks tend to perform well in an environment of

declining interest rates. Telephone companies may offer attractive long-term

growth opportunities, as they diversify and compete in recently deregulated

telecommunications markets.

Precious

Metals

Precious

Metals

Precious metals and the stocks of companies that mine and process them can be

affected by industrial and consumer demand, but the largest factor

contributing to volatility in this category is generally inflationary

pressure. Investors often flock to this category late in the expansion cycle.

Signals to Look for During a Business Cycle

A business-cycle trough. The trough is usually

characterized by low earnings and high unemployment. When inventories start to

shrink, an upturn may be on the way.

A business-cycle peak. Typically, earnings

are high and unemployment is low at a peak. When prices for raw materials rise

and inventories start to increase, look for a downturn to follow.

A bull market. A bull market is characterized

by rising price-to-earnings (p/e) ratios and falling yields. In its late

stages, a bull market may see high initial public offering (IPO) activity,

rampant speculative buying, and outperformance from small-cap stocks. A market

that seems indifferent to good news and shows a strong concern over interest

rates may be at its top. Because the stock market usually anticipates the

business cycle, it may begin to slide even as good earnings are still being

reported.

A bear market. A bear market is characterized

by rising yields, falling p/e ratios, and sharp declines with heavy trading

volumes. A market bottom, however, may be marked by indifference to bad news,

sluggish performance, and widespread pessimism. Upturns are often gradual and

imperceptible. If the market anticipates the business cycle, earnings may

continue to be weak for some time.

Other factors

Factors outside the business cycle

In addition to evaluating sector performance relative to the business cycle,

sector investors should also evaluate factors that are external to the

business cycle, as they can also influence the short- or long-term behavior of

various industries' stocks. Some of these factors include:

Government policies. Recent examples include

high-tech antitrust cases such as Microsoft*, the auction of radio

frequencies, the move to reform healthcare, and the approval or denial of

biotech new product proposals.

International trade and competition. The

increasing globalization of the economy means that foreign activities can

affect American markets. For example, China's move toward acceptance as a

member of the World Trade Organization could have a major impact on U.S.

exports. Industries that are sensitive to imports or exports will also be

affected by changes in currency values.

International exposure. When evaluating

sector funds, it is also important to keep in mind that certain sector funds

may invest in foreign securities. Similar to any mutual fund, a sector fund's

exposure to international securities could magnify the overall risk of the

fund. A good example would be foreign government regulation in the healthcare

sector. While some drug companies have benefited by government deregulation,

heavily regulated pricing and government bureaucracy has hampered others.

Consumer demand. While some aspects of demand

are tied to the business cycle, demand can also follow changes in

demographics, fashions, price levels, or cultural concerns. Strong holiday

sales (or the expectation of them) can send retail stocks up. During the late

1990s, the emergence of the internet and the demand for access created new

markets for internet service providers and on-line retailers.

Innovation. The introduction of new products

and technologies can change the entire landscape of an industry. Examples

include the booming trend toward wireless communication, and developments in

biotechnology. While great investment opportunities abound, rapid product

development can also lead to the obsolescence of established products.