|

Dr. P.V. Viswanath |

| Courses/Classnotes | ||

Basics of Valuation |

||||||||||||||||||||||||||||||

|

There are two basic approaches to Valuation:

However, one must recognize that all valuation is ultimately relative, and there are elements of relative valuation in discounted cashflow valuation as well, although this may sometimes be implicit. Spreadsheet templates applying the different approaches discussed here can be obtained from Prof. Damodaran's website. Some examples of equity valuation using these templates can be found at my classnotes website. Discounted Cash flow Valuation

where ke is the rate of return required by equity investors for the given level of equity risk embodied in the cashflows. Similarly, we could value the entire firm by taking all cashflows generated by the firm, and discounting them at the weighted average cost of capital: the market value weighted average of the rates of return required by the different security holders of the firm. Equity valuation models:Dividend Discount Model The Dividend Discount Model simply discounts the dividend per share at the required rate of return. In the general form of the model, the total life of the asset is divided into two parts: an extraordinary growth phase and a stable growth phase.

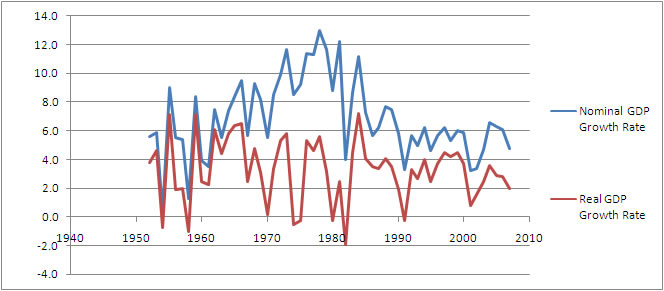

What can we take as the stable growth rate?

Figure: GDP Growth Rate of the US (Source: Bureau of Economic Analysis, http://www.bea.gov/national/index.htm#gdp)

What is the length of the high-growth period?

Expected Dividends during high growth periodWe first estimate the earnings per share for each year during the high growth period. This can be done usingThe following relationships can be useful in estimating expected earnings. the expected growth rate = retention ratio x return on equity;Return on equity is given by the identity: Return on equity = ROA + (D/E)[ROA-i(1-t)] whereThe return on assets can also be defined as After-tax operating margin x Asset Turnover Ratio, where

Expected Dividends in period t = Expected Earnings in period t x Payout Ratio in period t We can assume earnings growth to be Generally, payout ratios are inversely related to earnings growth rate. Firms with high earnings growth have low payout ratios, because one of the sources for the capital needed for growth is from the reinvestment of dividends. Finally, we need to estimate the terminal stock price. To do this, we need an estimate of the dividend for the year after the high-growth phase, and the stable growth rate. We should check that the fundamental estimates for the firm during the stable growth period are internally consistent. For example, we have the relation Growth rate in dividends/retention ratio = ROA + (D/E)[ROA-i(1-t)].In the stable phase, the growth rate in dividends must be close to the growth rate in earnings, otherwise the firm will either not be able to pay dividends after a while (if the dividend growth rate is larger) or it will have excess funds and a very low payout ratio. Hence the earnings growth rate, ROA, D/E ratio, etc. should be consistent with each other. FCFE Model:Free Cash flow is defined as the cash flow that the firm can afford to pay out as dividends. Many firms do not pay out all their free cash flow as dividends. This means that they are suboptimally carrying excess uninvested reserves; thus the dividend discount model may not capture their true capacity to generate cash flow for investors. The FCFE model estimates the value of equity as the present value of expected free cash flows to equity over time. FCFE is defined, in general, as FCFE = Net Income + Depreciation - Capital Spending - D Non-cash Working Capital - Principal Repayments + New Debt Issues. (Note: Non-cash working capital is used here rather than the broader definition of working capital for two reasons: one, cash is frequently not used for operational reasons; two, cash and cash-like assets and liabilities should be valued differently. Flows from cashlike assets and liabilities should, for obvious reasons, not be discounted at a risky discount rate. Hence cash should be added to the present value of FCFE, in order to get the total equity valuation. Interest-bearing short-term debt is also cash-like for our purposes, and is better included in financing considerations. Hence, in computing current assets for valuation purposes, we will exclude cash on the assets side and short-term debt (as well as the current portion of long-term debt) on the liabilities side. More information on this can be obtained on Prof. Damodaran's site. Working Capital usually changes in response to changes in revenues; hence it is best to forecast changes in Non-cash Working Capital in conjunction with revenue forecasts.) If net capital expenditures (i.e. capital expenditures less depreciation) and working capital are financed at the target debt ratio d , and principal repayments are made from new debt issues, then we have: FCFE = Net Income - (1-d )(Capital Expenditures - Depreciation) - (1-d )D Non-cash Working Capital, where d is the target debt ratio. Again, we have a similar valuation formula:

Once again, we can allow for a high growth phase and a stable growth phase.

We start out with estimating earnings per share, and the growth rate in earnings, as before. We then adjust Net Income by the net capital expenditures, working capital needs, and debt-financing needs. Net capital expenditures and working capital will need to be high for high growth rates to be maintained. Normally, high growth firms are also high risk, and debt is difficult to obtain at reasonable rates. Hence leverage ratios are low for such companies. As growth tapers off, leverage ratios usually go up. The terminal stock price is estimated using stable period estimates of cash flow, net capital expenditures and working capital needs. Again, consistency is required in the numbers assumed. The FCFE method will produce different results from the Dividend Discount method if retained earnings are not invested optimally. In particular, if funds are invested in negative NPV projects, the FCFE method could provide higher estimates of value than the Dividend Discount method. On the other hand, if current dividends paid are too high and at unsustainable levels, then securities will have to be issued at high cost to finance the dividends. In this case, the Dividend Discount method will show an ostensibly higher stock value, but one that is not warranted. The key to the value obtained under the FCFE method is in the assumptions that are made regarding capital expenditures and other fundamental variables. The Dividend Discount model is more passive regarding managerial options. If the market for corporate control works well, a higher FCFE method value will eventually lead to a takover, but in the short run, the dividend discount model may not provide a good estimate of value. FCFF Valuation:The Free Cash Flow to the firm can be computed as the sum of the cashflows to all claimholders. FCFF = Free cash flow to equity + Interest expense (1-t) + Principal Repayments - New Debt Issues + Preferred Dividends. Alternatively, from a more direct point of view, FCFF = EBIT(1-t) + Depreciation - Capital Expenditures - D Non-cash Working Capital The differences between FCFF and FCFE arise from cash flows associated with debt -- interest payments, principal repayments, and new debt issues -- and other non-equity claims such as preferred dividends. Growth in FCFE versus growth in FCFF. The primary cause of differences in the growth rates in FCFF and the FCFE is the existence of leverage. Leverage increases the growth rate in the FCFE, relative to the growth rate in the FCFF. We can see this from the identity gEPS = b[ROA + D/E(ROA-i(1-t))]. (b is the retention ratio.) If ROA > i(1-t), then a higher leverage ratio implies a high growth rate in earnings per share and correspondingly in FCFE. On the other hand, the cashflow to the firm is not affected by leverage. The growth rate in EBIT, which effectively determines the growth rate in FCFF will generally be lower and be equal to the product of the retention ratio and the book return on assets. Again, a high growth phase and a stable growth phase are allowed for. The valuation formula is:

As in the FCFE method, we need the following steps:

This method is easier to apply where cashflows to debt are not smooth and vary over time. At the same time, the firm valuation approach does require information about debt ratios to generate an estimate of the weighted average cost of capital. The two techniques will provide similar equity valuation numbers if the two conditions are met:

Estimating Change in Non-Cash Working Capital

This essentially involves utilising existing valuations of 'comparable' assets to price a given asset by working with a common variable such as earnings, cash flows, book value or revenues. Examples:

One way to avoid making too many assumptions regarding the comparability of firms is to use equations relating the multiple to fundamentals. For example, for a stable growth firm, the Gordon Growth models tells

us: Using multiples depends heavily on assumptions regarding what is comparable. Furthermore, any error that the market has made in valuing the comparables will be carried over the valuation of the firm under consideration. (based on Damodaran's Corporate Finance, chap. 23.) |